African startups raised over $1.5 B in H1 2026 as equity stages a comeback

African startup funding reached $1.5 billion across 137 deals in H1 2026 as equity rebounded, Kenya led funding, and Nigeria lagged in capital raised.

Between January and June 2026, 137 deals were recorded across the African startup scene, totaling approximately $1.5 billion in disclosed funding, according to Condia’s funding tracker. The numbers reveal an ecosystem mid-swing from debt back to equity, particularly in the last two months of the half. Growth-stage companies are still pulling in the largest rounds, and Nigeria is falling short of the “Big Four” markets, posting more deals but far less money.

The debt-to-equity swing in Q2 2026

The arc signal in the Q2 2026 data is the return on equity. Of the 70 deals tracked between April and June, 46 were pure equity and four combined equity and debt, more than two-thirds of all deals in the period.

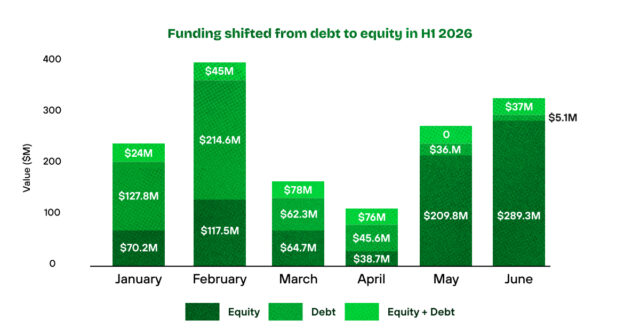

In Q1 2026, debt was the dominant instrument. January and February were each driven by debt, accounting for more than half of its total funding. By May and June, debt’s share had collapsed to under 15% as equity rounds like Paymentology’s $175M raise and Spiro‘s two rounds of $215M and $55M took over. This shows that investors are still willing to back growing industry leaders.

To sum H1 2026 up: pure equity raised $790.3M across the half, while debt and hybrid (equity-and-debt) instruments accounted for $751.5M combined. In April specifically, debt and equity were roughly equal, while mixed equity-and-debt rounds were the largest single category that month. By the end of H1, equity had clearly outweighed pure debt, totaling $790.3M versus $491.5M. On average, though, debt rounds were the bigger bet: $14.5M per debt round versus $10.8M per equity round. Debt just had fewer rounds to work with.

In H1 2026, monthly totals, especially in Q2, can make it look like the market is gaining momentum, but a closer read shows it is built on one mega-deal at a time rather than broad-based growth. Across April, May, and June, the top three deals accounted for 55%, 85%, and 94% of each month’s total funding, respectively.

Read also: Stablecoins dominate as African startups raise $53 million in May

Quality, not quantity, as Kenya leads and Nigeria lags

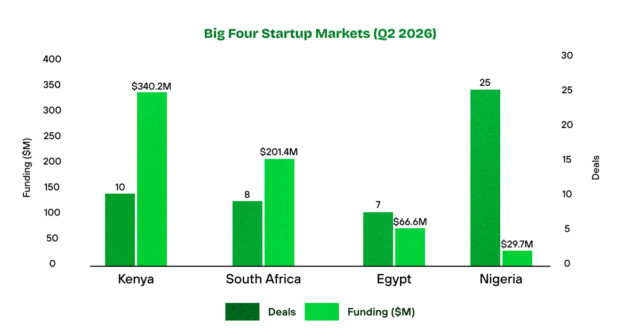

Nigeria remains the most active market by deal count, with 25 of the 70 Q2 deals, but the least paid, as 36% of deals totaled just 4.0% of Q2’s disclosed funding, or $29.7M. Its average disclosed deal size was about $1.6M, the smallest among major markets. This points to a market rich in early-stage activity but starved of growth-stage funding.

This weakness was even more pronounced in Q2 than in Q1 2026, when it was $7.2M.

Kenya, on the other hand, took nearly half of all Q2 funding, with $340M from 10 deals. That is largely down to Spiro, the Kenya-based EV battery-swap company, which alone raised $270M combined in two rounds.

In total capital raised, Nigeria fell behind the other three “Big Four” markets: South Africa raised $201.4M across 8 deals, and Egypt raised $66.7M across 7 deals. South Africa came in second on the strength of a dominant May, in which it raised $185.9M across just 3 deals — its biggest month of the year.

Angola, Rwanda, Tanzania, and Tunisia all made their debuts in Q2, while Togo and Senegal were last seen in February and March, respectively.

Read also: Africa’s startups have raised over $700 million in Q1 2026. Here’s what the numbers say.

Mobility is coming for FinTech’s top spot

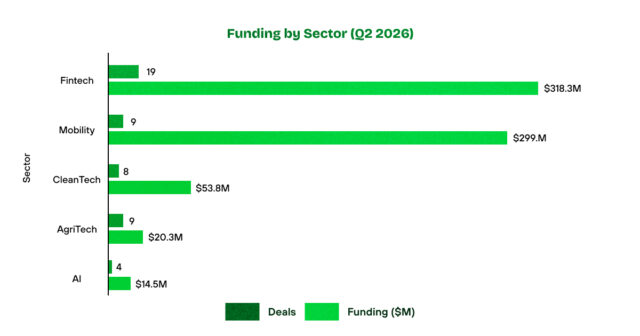

In Q1 2026, FinTech led by a wide margin in both deal count and total amount raised (23 deals, $292.1M, versus Mobility’s 10 deals, $161.2M). Now Mobility is closing the gap. In Q2 2026, FinTech still led on deal count with 19 deals worth $318.3M, but Mobility nearly matched it in dollar terms with $299.9M from 9 deals. Mobility’s average disclosed deal size of $33.3M dwarfs FinTech’s roughly $19.9M.

AgriTech edged out CleanTech on deal count in Q2, 9 to 8, but AgriTech raised less, at $20.3M, though that is a sharp improvement on the $6.5M it attracted in Q1. CleanTech, meanwhile, fell hard, from $170.3M in Q1 to $53.8M in Q2.

Another sector to watch is AI, which logged 4 deals worth $14.6M in Q2.

A change of weather in June

June had the highest deal count at 28, narrowly ahead of April’s 27, while May had just 15, the lowest of any month in the entire first half of the year. June’s $331.4M in total funding was also more than double April’s $160.3M.

June’s deal count was inflated by Cascador‘s June 4 cohort of 7 investments, announced in a single announcement, making it the most active lead investor in H1 2026, followed by Madica (3 deals, announced April 8) and Village Capital (2 deals, announced May 6).

June’s funding rush also aligns with the mid-year reporting season and major mid-year business summits, which often serve as backdrops for funding announcements, and some funds align their budgets with an April-to-June fiscal year.

Adding to all of this, the funding landscape saw several repeat raisers in H1 2026: Spiro (4 rounds, $327M), MNT-Halan (2 rounds, $41.3M), Terra Industries (2 rounds, $33.75M), and Max/MAX (2 rounds, $32M).

Data sourced from the Condia funding tracker, covering deals announced between January 1 and late June 2026.