EXCLUSIVE: Sycamore transitions to financial services group, following Microfinance Bank (MfB) licence

Sycamore, with ₦50 billion AUM, now operates three regulated businesses, lending, asset management and its own savings & deposit-taking product via microfinance bank licence

Sycamore has fully transitioned from a digital lender to a group operating three regulated financial services businesses.

In 2025, the Lagos-headquartered group generated about $5 million in revenue and processed $73 million (₦100 billion). It also manages $36 million (₦50 billion) in assets while serving over 400,000 customers (individuals and SMEs) across various Nigerian states and countries.

The Microfinance bank is the final piece of a structure the company has been assembling since it secured a Securities and Exchange Commission (SEC) licence for asset management in March 2025.

“When we started Sycamore, lending was the entry point, but the plan was always to build a financial services company that could serve a customer across their entire financial life. The Securities and Exchange Commission (SEC) licence gave us the asset management capability, and now our microfinance bank provides the banking infrastructure. For the first time, a customer can borrow, invest, save, and transact within one group that we fully operate,” said Babatunde Akin-Moses, Sycamore Group CEO.

Sycamore group now comprises three entities offering products like salary loans, business financing, investments, asset portfolios, and multi-currency wallets.

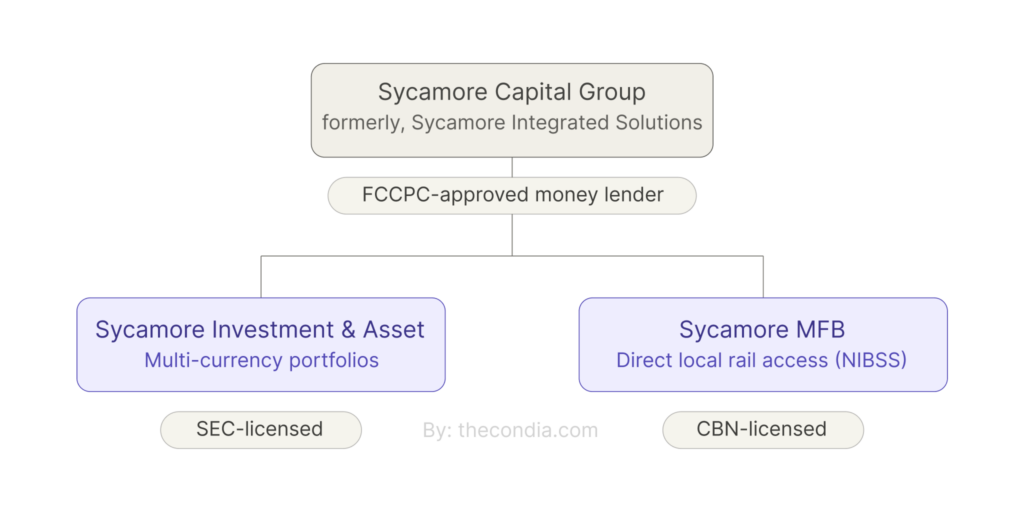

First, Sycamore Integrated Solutions Limited (SISL), the flagship consumer lending business, which is approved by the FCCPC as a Digital Money Lender. It was the first Nigerian fintech to secure this status in 2022. This entity continues to hold multiple State Money Lender licences while restructuring to become the parent company, renamed Sycamore Capital Group.

Second, Sycamore Investment and Asset Management Limited (SIML), licensed by the Securities and Exchange Commission (SEC), manages diversified portfolios in local and foreign currencies. SIML offers stocks, bonds, and money-market instruments in both naira and foreign currencies. Its USD-denominated investment product is already live, providing Nigerian investors with a regulated channel to hold and grow their wealth in dollars.

This month, Sycamore Microfinance Bank joined the fray, providing the company with its own banking infrastructure, including a direct connection to the Nigeria Inter-Bank Settlement System (NIBSS).

Sycamore’s unconventional path to fintech supremacy

MBA students, Babatunde Akin-Moses (CEO), Onyinye Okonji (then CMO, now CCO), and Mayowa Adeosun, at the Lagos Business School, founded Sycamore in 2019. “During one of our semesters, we were looking at problems facing MSMEs, and we realised that SMEs struggle to find access to affordable financing,” Akin-Moses told Condia, formerly Benjamindada.com, in 2022.

It was coming on the scene at a time when several VC-backed startups, like FairMoney, had raised millions of dollars to scale their lending products. However, the lending market is such that customers continuously hop around in search of the best interest rate and hopefully, “free money”. So, retention is low, customer lifetime value is cut short, and in cases where lenders are not able to recoup their funds, non-performing loans increase.

Sycamore did a few things differently. First, it did not chase growth-at-all-cost, often referred to as blitzscaling in the world of startups. The company did not buy a microfinance bank from the outset, as most well-funded players did. Instead, being scrappy, it went after state money lender licenses in its key hubs, including Lagos, Abuja, Port Harcourt, Ibadan and Abeokuta. Also, unconventionally, it did not give instant loans. “Sycamore is not an instant loan provider. There is a high default rate on instant loans…” Adeosun told Condia in 2022.

When it was time to earn from float, the company opted for an SEC asset manager licence instead of a microfinance bank, which could allow them bundle deposit-taking and lending activities under one umbrella while earning net interest income. Okonji said, “We chose to build each business under its own licence and regulatory framework rather than trying to stretch one licence across multiple services. It takes longer and costs more, but it means every part of what we offer sits on its own regulatory foundation. That matters to the kind of customers we want to attract, especially on the investment side, where trust in the regulatory backing of a product can determine whether someone commits their money [emphasis mine].”

Furthermore, on capitalisation, the company tapped into awards like the NSIA Prize for Innovation, where it won $100,000 in 2024. It also leveraged alternate financing, and local commercial paper issuance to raise naira-backed debt, making its repayment less susceptible to foreign exchange swings and naira devaluation. In 2025, it structured a ₦1.5 billion debt financing (< $1 million) deal with Cascador Catalytic Fund, after participating in the latter’s pitch day.

EVENT: Join Cascador Programme Director, this evening, for an online webinar on alternative financing for African startups, moderated by Condia.

What does Sycamore’s Group structure mean for customers?

Customers still use the same Sycamore app. However, the different services like loans, investments will be powered by multiple subsidiaries, under the hood. In addition, customers will have a better product experience as Sycamore connects directly to NIBSS for granular transaction lifecycle control, cheaper access to electronic funds transfer, and listing as a deposit-taking institution on the bank beneficiaries list. Thus, customers will now receive personalised Sycamore-branded account numbers.

A direct benefit is free inward transfers to those accounts, and the removal of the previous ₦3.75 million cap on card and online payments, according to a statement shared with Condia. In addition, a single customer can now get loans of up to ₦100 million.

Managing Director, SIML, Gbenga Magbagbeola said, “Owning the banking infrastructure was a prerequisite for what we’re building across the group. When your asset management platform needs to process redemptions instantly, or your lending business needs to disburse within minutes, you need to control the processing queue yourself. The MFB gives us the speed and reliability across all three businesses that we could not guarantee when we depended on a partner bank.”