Why debt must be part of every African startup’s 2026 financing strategy

Equity built Africa’s startup ecosystem but in 2026 the founders who scale will be the ones using debt as part of their financing strategy.

Historically, most African tech startups avoided debt because it was expensive, hard to access, and unattractive for such a high-risk business. That framing no longer fits.

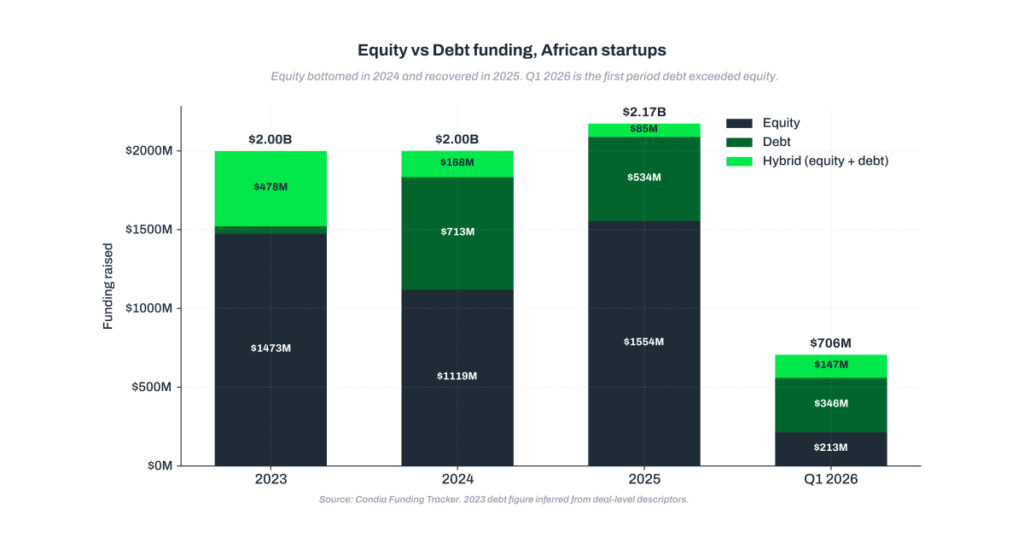

The first quarter of 2026 continued a trend that Condia’s funding tracker first flagged in 2025, pointing to a broader shift in Africa’s startup funding ecosystem. The largest African startup financings in 2025 and early 2026 have been debt rounds for mature, cash-flow-generating companies.

Debt and hybrid instruments accounted for $490M of the quarter’s $705M total. Meanwhile, equity funding fell 39% year-on-year, from $348M in Q1 2025 to $213M in Q1 2026.

This marks the first period on the continent in which non-equity capital exceeded equity in both share and volume. Mature startups in sectors like energy, mobility, and fintech are using debt as a cost-effective tool to scale infrastructure and deepen market penetration rather than to survive.

This also indicates that the largest investments are now concentrated in growth-stage companies that have moved beyond proving a concept to demonstrating scale.

Why debt financing is rising in Africa’s startup ecosystem

Margaret Ntambi, the Managing Partner at Velocity Digital, argues that the rise of debt financing in Africa signals market maturation rather than a replacement for equity. She notes that developed markets like the US already offer founders multiple options, including venture debt, bank lines, and private credit, and Africa is beginning to follow that path as data from reports like Condia and Partech show.

For context, the UK tech ecosystem raised $7.5 billion (€6.4 billion) in Q1 2026, a 32% increase from the $5.7 billion raised in Q1 2025, according to data intelligence platform Tracxn. Meanwhile, in the US, technology companies issued a record $108.7 billion in corporate bonds in the final quarter of 2025, per Moody’s Analytics data.

Related Post: Is debt financing ideal for African startups in a funding winter?

Debt is now flowing to companies with strong cash flows, quality reporting, and repayment capacity, such as SunKing in cleantech. For early-stage founders, the focus should be on matching financing type to business stage rather than defaulting to equity. “Debt is becoming more available, specifically for companies that are earning for this type of financing. The better question is what kind of financing should you get, depending on what stage you’re in building your business.”

Marge explains that Africa has historically been overly dependent on equity, but this is changing as structured capital becomes accessible. Debt financiers are now underwriting businesses based on cash flow strength, reporting quality, and repayment discipline.

She suggests that during product discovery, customer acquisition, and early team building, equity remains appropriate, while debt or hybrid options make more sense for financing receivables, inventory, and asset deployment. Overall, she sees this shift as giving founders more freedom to choose the right financing mix for how they are building their business.

Choosing between debt and equity

The debate between debt and equity is one that every founder eventually faces as the financing landscape tilts toward one or the other. Debt financing reached a record $1.64 billion in 2025, accounting for 41%-46% of total capital deployed.

While equity remains essential for early-stage product discovery and team building, debt is now preferred for growth-stage companies with predictable revenue streams to fund working capital, inventory, and liquidity without diluting ownership.

Related post: How to secure alternative financing for your business in 2026

According to Babajide Duroshola, a seasoned operator who has raised ₦98 billion in debt facilities, the answer is not one or the other. “It is a little bit of both at the end of the day,” he says. The distinction, however, matters enormously. Equity, Duroshola explains, is for proving a concept and building a team. Debt serves an entirely different purpose. “Debt is there to scale an already working business idea. It is not there to test a prototype or find product market fit.”

In other words, if you are still figuring out whether your business works, debt is the wrong tool. It only makes sense once the business has demonstrated that it works and simply needs fuel to grow further.

This is why Duroshola describes debt as a working capital tool rather than an expansion vehicle. “Equity allows you to invest in technology, expand into new markets, and do all of those things. Debt allows you to cover operational costs.”

The difference is subtle but critical. When you take on debt, repayment is guaranteed, and it comes with interest. That changes how you have to think about your pricing. “If it costs you 10 naira to service the debt, you have to build that 10 naira into your pricing,” Duroshola says. “For every new sale you generate, you are also paying the cost of servicing that debt.”

When can a startup explore debt funding?

Debt funders evaluate startups through a fundamentally different lens than equity investors. While a venture capitalist asks “how big can this get?”, a debt funder asks “what is the worst case scenario, and do we still get paid back?” Every criterion they apply flows from that single question.

The most essential thing a debt funder wants to see is evidence that you can repay. This is why recurring revenue is so attractive to them. Monthly and annual recurring revenue is predictable and contractual, giving a lender confidence that repayments will not disrupt the business.

Furthermore, they look hard at gross margins and unit economics, which is profitability at scale. A business burning through cash faster than it earns is a red flag, not because growth is bad, but because debt repayments must fit within real monthly cash flows without threatening the company’s survival.

Duroshola puts it plainly. “The more output you generate against the dollar you are pricing at, the more likely you are to hit profitability.” And that, he says, is precisely what debt funders are looking for.

Margin is the clearest proof of that. Duroshola draws from his time at SafeBoda to illustrate the point. “We were losing about 19 cents a ride, which meant we weren’t making any margin at all. No bank was going to put money into that kind of business.

They would tell you that you are just pissing the money away.” But flip that around, and the conversation changes entirely. If SafeBoda were making 19 cents on every ride, there is cash flow, there is a basis for repayment, and suddenly, debt makes sense.

“These people are making money,” is how a lender would see it. “They have cash flow that allows them to repay their loan when the time is right.”

Pursuing the right financing for your businesses

Many founders in African markets are not adequately sensitised to how debt works or how to use it well. Some of this stems from cultural and religious discomfort with borrowing, yet the reluctance, wherever it comes from, can be costly. Used correctly, debt can be enormously profitable for a business.

A distinction Amanda Etuk, the Program Director of Cascador, made is between working capital financing and capital expenditure financing. They are not the same conversation, and conflating them leads founders into trouble. “There is a difference between raising working capital and raising to buy a machine,” she says. The type of financing you pursue should match what you actually need the money for.

Related post: The Moove pitch that became a debt trap for Lagos drivers

Then there is the uncomfortable reality of the Nigerian lending environment. Commercial banks are difficult to access, with collateral requirements that Etuk describes plainly as not for the faint-hearted. The alternatives that are easier to access often come with interest rates of 4% to 6% per month, which, when stacked against the margins most businesses actually make, create a serious problem.

“If your margins are maybe just 30% per annum, you have no business taking debt at the interest rates that are common with a lot of microfinance banks today,” Etuk says. The message is clear. Before any founder reaches for debt, they need a firm grip on their unit economics and margins. “You have to really have a handle on your finances before you do so.”